Klend features:

- Unified Liquidity Market

- Elevation Mode (eMode)

- CLMM LP Tokens as Collateral

- Poly-linear Interest Curve

- Protected Collateral

- Auto-deleverage

- Asset Tiers

- Real-time Risk Simulator

- Advanced Oracle Risk Engine

- Soft Liquidations

- Dynamic Liquidations

Unified Liquidity Market

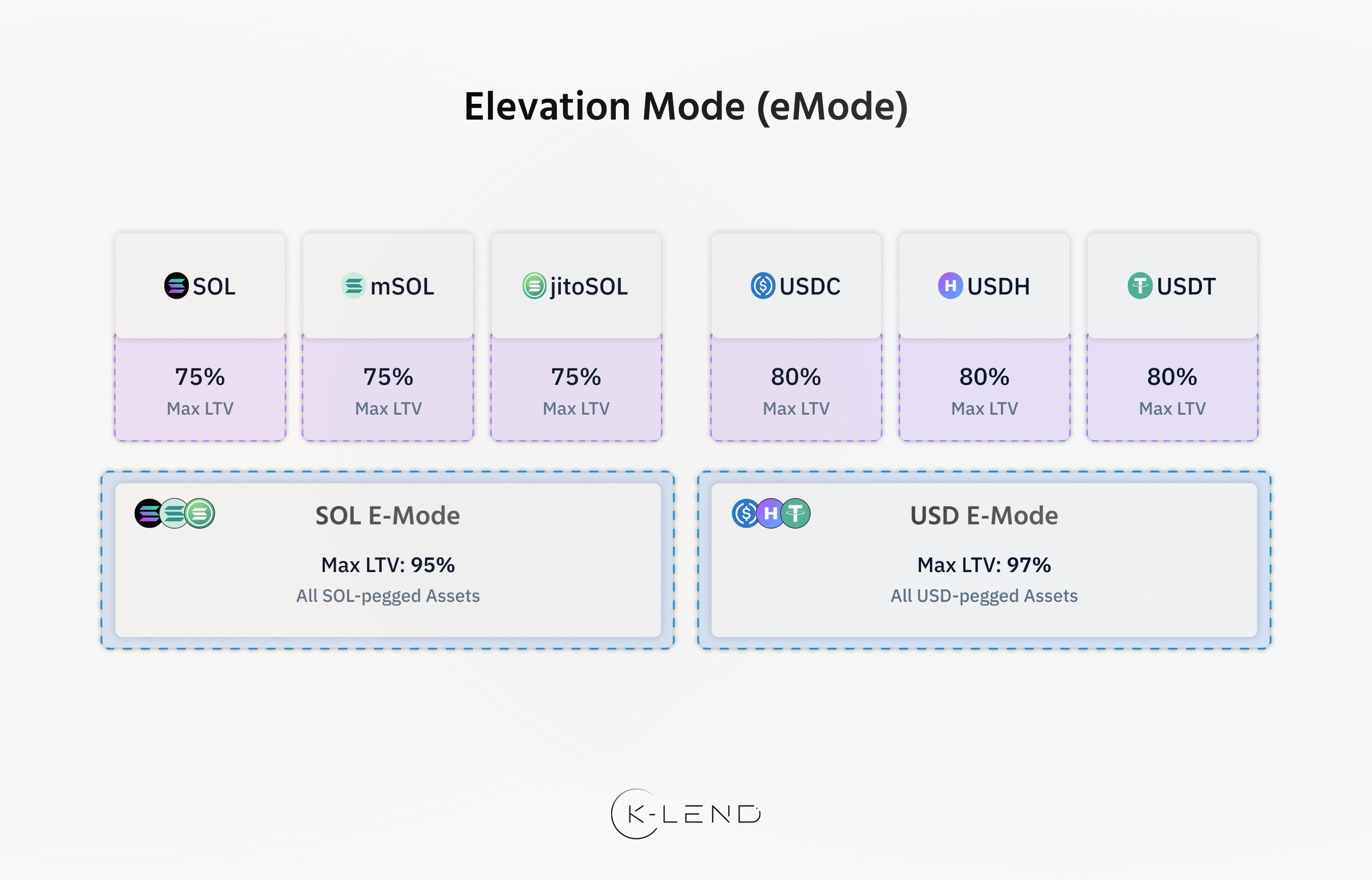

Klend features a single liquidity market, rather than a multi-pool design. Within this market, Klend introduces an ‘eMode’ mechanism that enables higher leverage when lending/borrowing solely within a certain asset grouping. Multi-pool designs have shown to be inefficient in lending protocols, fragmenting liquidity and ultimately leading to lower utilizations and lower yields for lenders. In practice, the primary benefit of a multi-pool design is that each isolated pool (i.e. different asset combinations) can have custom parameters, while separating risk from the main liquidity market. However, Klend’s risk engine allows for risk isolation even within a unified liquidity market, while the protocol’s eMode infrastructure enables customized asset parameters within a single market.Elevation Mode

Elevation Mode (first introduced in Aave V3 as Efficiency Mode) allows users to borrow highly correlated or soft-pegged assets at a more capital-efficient LTV ratio. Within Klend’s unified liquidity market, assets can be grouped into “elevation groups (eGroups)”. Each eGroup can have customized LTV parameters and liquidation thresholds assigned to it, ultimately unlocking higher leverage possibilities, as well as tailored liquidation parameters. Crucially, elevation groups are built into the main liquidity market. All Klend users can thus access the unified liquidity market, while eMode empowers them to attain greater capital efficiency and higher leverage via customized asset parameters. For instance, if all SOL and SOL LST tokens are grouped into an eGroup with a 95% max LTV, all the tokens will adopt 95% as their new max LTV. Any supply/borrowing within this asset grouping can then be done at this LTV, allowing for increased capital efficiency and leverage between these assets.

CLMM LP Tokens as Collateral (kTokens)

The growth of Uni V3 and concentrated liquidity as DeFi’s primary liquidity model has virtually stopped leveraged LPing in its tracks. This is because LP positions from CLMMs are non-fungible, and cannot easily be used as collateral nor levered up. Kamino’s automated liquidity infrastructure already tokenizes CLMM LP positions. These positions, called kTokens, are fungible, easily liquidatable SPL tokens. Klend supports these kTokens as collateral, allowing users to use leverage by borrowing against / looping their LP positions.Poly-linear Interest Rate Curve

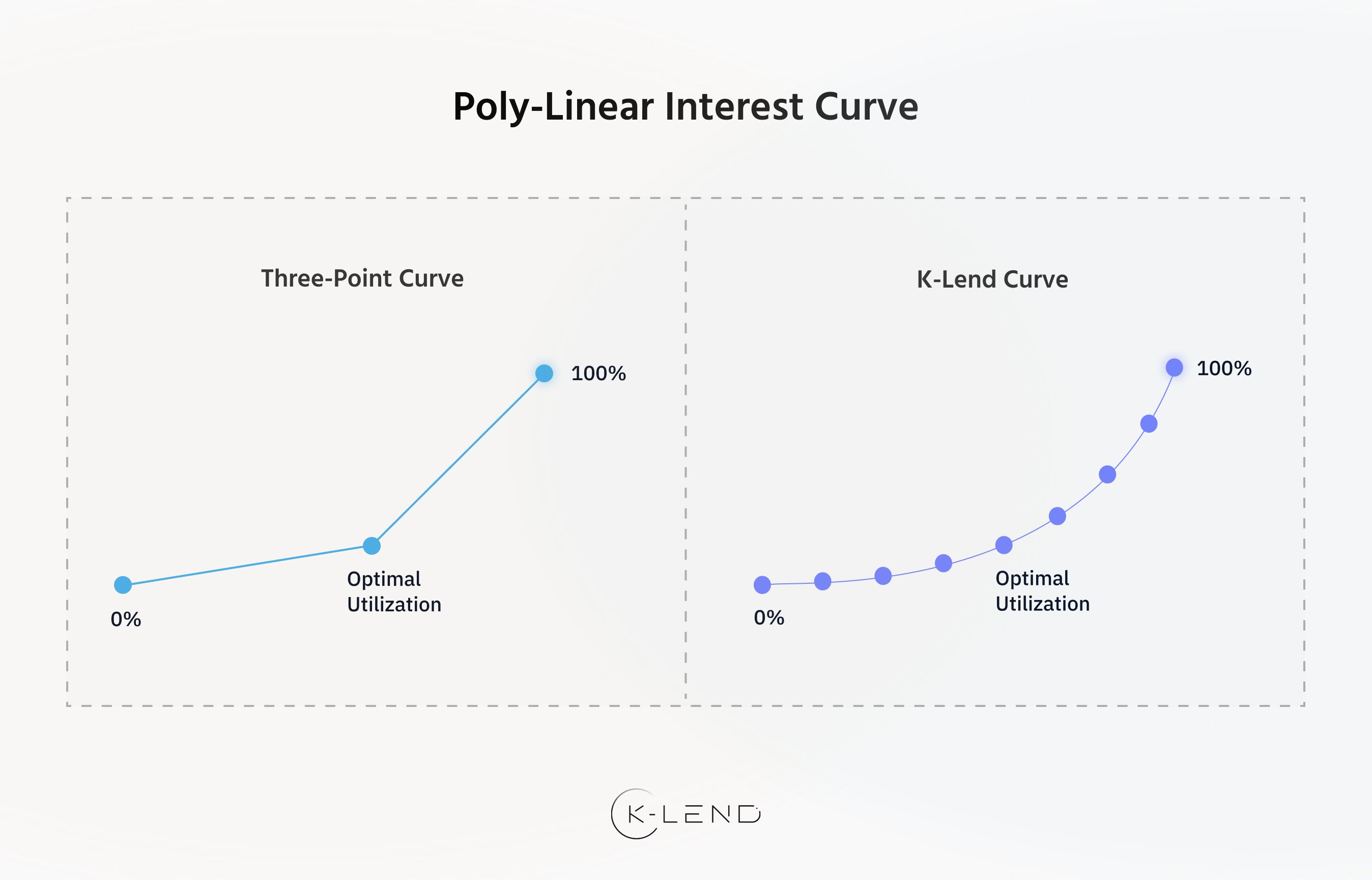

Interest rate (IR) curves dictate supply and borrow rates based on an asset’s utilization rate. Interest rates are intended to keep markets at an equilibrium, while ensuring lenders are able to access their liquidity should they wish to withdraw capital. A multi-point IR curve reduces shocks to the system by more gradually increasing or decreasing rates when necessary. With theoretically up to 11 points on its IR curve, Klend provides a major improvement over traditional 3-point curves in other lending markets. This is beneficial to borrowers who are subject to more gradual rate increases before repaying their debt.

Protected Collateral

On Klend, users can opt to keep their collateral assets from being borrowed by other users, thus protecting their assets from any borrower default risks. Such assets, referred to as “Protected Collateral”, can still be used as collateral for borrowing by the depositor, but they do not earn interest on these assets. Protected collateral can be withdrawn at any time.Risk Management

Deposit Caps

Each asset on Kamino Lend is subject to a deposit cap, ensuring that the system contains a safe amount of any asset at any given time based on the asset risk score, which takes into account various risk metrics, such as the available market liquidity, the volatility of the asset, the security risk of the asset etc. These caps are continuously monitored and are subject to readjustments if deemed necessary.Borrow Caps

Similarly, borrow caps limit the borrowing of each asset to a certain amount, based on the asset risk score. This is continuously assessed and subject to change if deemed necessary.Auto-Deleveraging

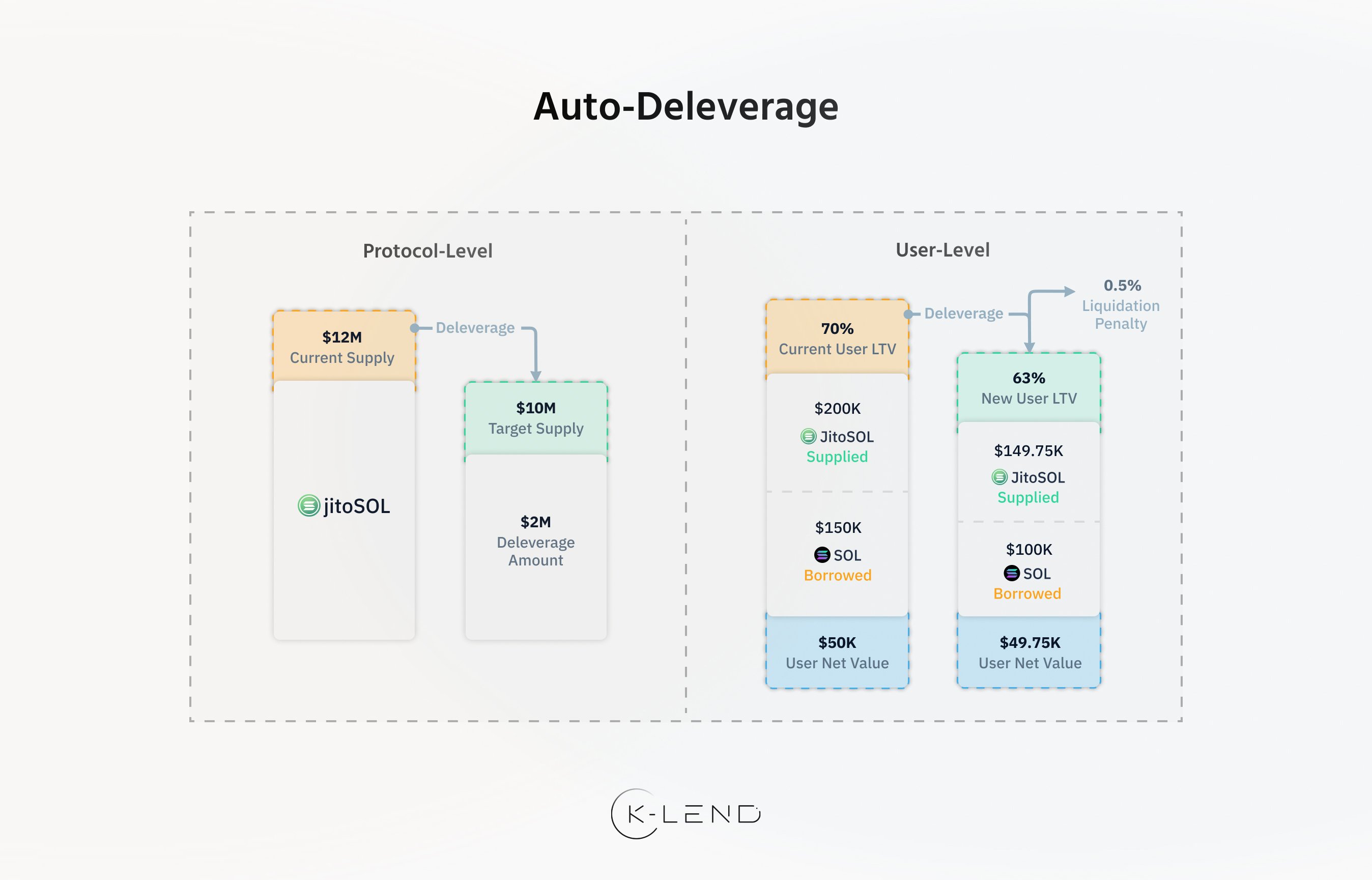

Kamino’s auto-deleverage mechanism lowers the deposit and/or borrow caps of a certain asset to an amount that is deemed safe considering current market conditions. Lowering the caps thus triggers an automated unwinding event. If an auto-deleverage event is triggered on USDH deposits for example, users are notified via Kamino’s communication channels, and given a specified period to adjust any positions using USDH as collateral. Once this period elapses, the system begins partial deleveraging of loans backed by USDH, starting with loans closest to liquidation. Deleveraged loans incur a minor liquidation penalty which escalates continuously up to a maximum, until the target collateral/borrowing amount is achieved. Users subject to deleveraging will see a proportional reduction in the target asset, along with the corresponding tokens in the position, generally resulting in a more healthy Loan-to-Value (LTV) ratio.

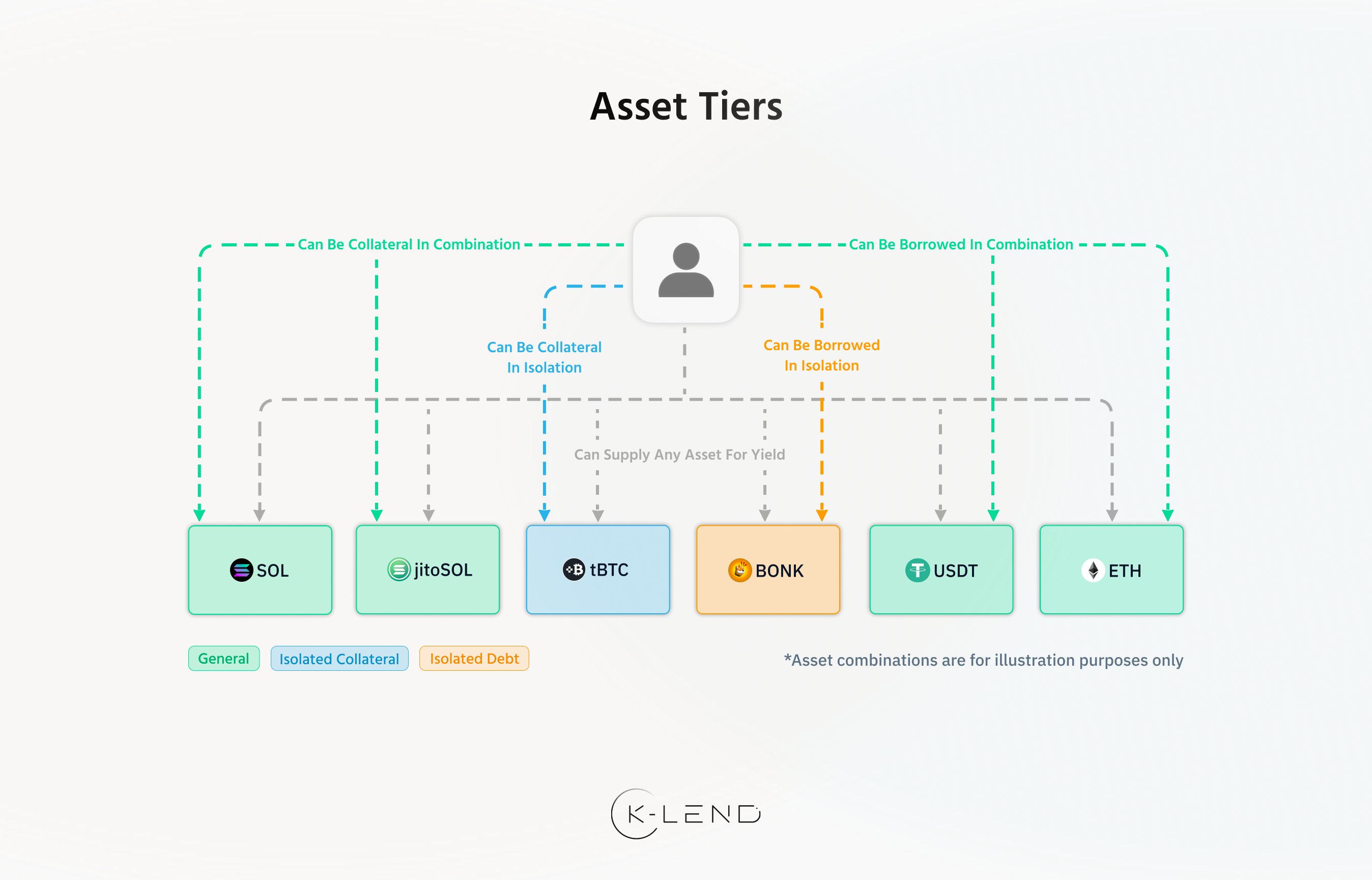

Asset Tiers

A unified liquidity market offers considerable benefits to borrowers and lenders, but it also presents new challenges to risk management. Risk can easily spill over from one asset to another, ultimately increasing the risk of bad debt on the protocol. Klend will introduce Asset Tiers to ensure that users can borrow and lend a wide range of tokens safely, without fracturing liquidity between isolated pools. A tier-based system allows the protocol to offer permissionless borrowing and lending for any token on Solana, with Kamino’s Risk Council determining the ways an asset can be used on the protocol, grading each asset into one of three categories: Isolated Debt, Isolated Collateral, and General.Isolated Debt

Can be borrowed, but only in isolation from other assets. These assets cannot be used as collateral, but can be supplied for lending yield.Isolated Collateral

Can only be used as collateral, and only in isolation from other assets. Isolated Debt assets cannot be borrowed against Isolated Collateral.General

Can be used as collateral to borrow other assets, and can be borrowed alongside other general assets. This will typically represent the most liquid assets on the network.

Borrow Factors

Borrow factors (BFs) are risk-adjusted borrow values assigned to each asset on Klend. This determines the borrowing capacity of a debt asset within a loan, based on its Asset Risk Score. This is parallel to loan-to-value ratios (LTVs), which indicate borrowing limits from the collateral asset perspective. Klend combines LTV and BF to express a weighted borrowing capacity based on the asset composition of a position. This allows the protocol much more flexibility in assessing the risk of each position on the platform. For example, let’s assume you want to supply $100 of SOL as collateral and borrow either USDC or BONK:- SOL is a widely circulating collateral asset, and its maximum LTV ratio = 80%

- USDC is deemed a less risky asset than BONK.

- USDC Borrow Factor = 1

- BONK Borrow Factor = 2

- Borrow capacity is expressed as: (Collateral Amount * Collateral LTV) / Borrow Factor

- USDC borrow capacity against SOL = (80

- For BONK, due to a BF of 2, you can borrow up to $40.